I believe we are at a critical juncture on two interrelated approaches to data sharing. I am not sure we are having the right conversations in the right places, and I wonder if we are asking the right questions as industries, as governments or as citizens.

What are our data strategies and how should we discuss their framing?

For this conversation, I’d like to avoid deep dives on ‘personal data’ issues but rather focus on the general principles of the collisions between market behaviours and the open web. It feels like echoes of the ‘AOL/MSN vs the open web’ approaches from the 1990s, but evolved through the 25-year lens of how that all played out.

1. Web-scale codification of our financial systems

The first is ‘Open Banking’ — a new regulation that mandates interoperability and data portability between banks and others. This fundamentally addresses two big areas: (a) consumers — it mandates customers own and can control their data and (b) businesses — it defines the whole-market rules for data sharing and how this interfaces with a regulatory environment. These serve to address everything from data rights to security, from user-experience to liability transfer. Ultimately it should be beneficial to all actors in the system: reducing transactional friction, reducing costs and increasing functionality.

This work is being taken further: ‘Open Finance’ could extend the framework of Open Banking across finance (pensions, insurance, investments) and beyond the sector (e.g. energy, health). The UK Open Banking Standard is itself openly licensed in content (Creative Commons) and code (MIT).

As ever with such initiatives, there are predictable market moves to try and create new monopolies, or simply arrive at ‘less open’ outcomes. Some are easy to see (VC is pouring in, to ‘own the platforms’); some are harder to understand or nuanced (how countries should be careful to define what ‘open’ means). Done well, I think we could unlock huge value while better protecting both people and businesses. Done without care, I think we could stifle innovation, allow new monopolies to emerge and create a more brittle economy.

How should we frame a conversation around things that could undermine what — in my opinion — could be the first ‘web-scale’ regulatory codification of our financial systems?

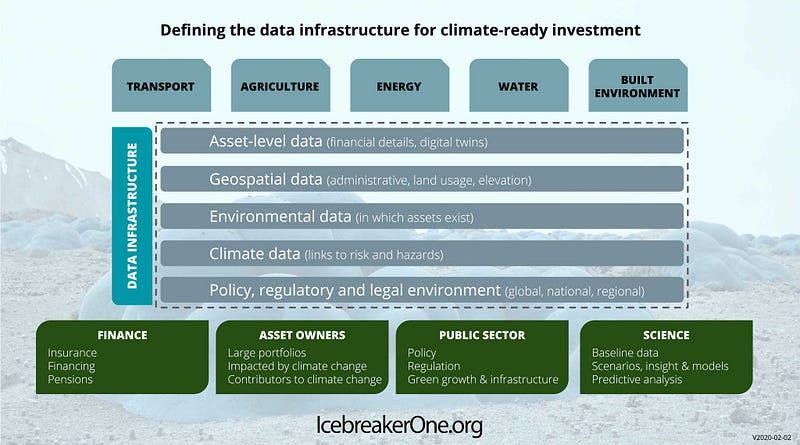

2. Designing the data infrastructure for a climate net-zero future

The second is the climate emergency. We have just launched a new non-profit to extend the principles of open finance across many sectors to empower everyone to act.

Within it, we’ve started to define the ‘data infrastructure’ for ‘climate-ready investment’.

Such an approach could enable everything from asset-level information to energy, policy to investment to interconnect.

I’ve often thought of the web as a social response to globalisation. It feels to me as if our climate (and related biodiversity) crises may be realised as the purpose for which we need the web of data — for it to finally mature and become a reality, driven by our collective needs. Much as Tim said ‘this is for everyone’, our climate emergency could now be embraced as — this needs everyone.

Can we navigate towards a wealth of outcomes rather than just outcomes of wealth?

And so to framing questions:

- How do we promote focus (and challenge) around open, federated market development? (ie. the open web not ‘sort of open’ ecosystems)

- How do we define ‘open’ properly in the context of ‘open standards’ that cover all the non-tech components? (e.g. ‘open license’ vs ‘royalty-free’)?

- How can we help companies see openness as a driver of commercial benefit, not a threat? Open markets can drive growth, increase efficiency and reduce risk, but the tendency is always to ‘pull up the drawbridge’ when a castle is built in an ecosystem—or tightly cooperate in a closed market.

- How can we talk about data without talking about technology?

- How do we frame constructive and practical narratives around our data-sharing economy that drives us to outcomes rather than the usual rabbit holes of ‘social good’ vs ‘commercial value’ vs ‘exploitation’?

- How can we focus on solving specific problems, working out the potential issues as-we-go and act to resolve them in a way that is ‘good enough’?

- Should we talk about data rights rather than ethics?

NB: I co-chaired the development of the UK’s Open Banking Standard, have input into the FCA Open Finance group and have been working with Canada and New Zealand on their approaches. I also participate in the FCA/PRA Climate Financial Risk Forum and am the founder of both Dgen.net and IcebreakerOne.org.